Can you finance a car with bad credit? Yes, absolutely. Getting auto financing with poor credit is possible, even if your credit score is low. It might be harder than with good credit, and the terms might be different, but people with bad credit car loans get approved every day. This guide will show you how to find lenders and improve your chances of getting car loans for low credit scores.

Image Source: www.credit.com

Why Your Credit Score Matters

Your credit score is like a report card for how well you handle borrowing money. It tells lenders how likely you are to pay back a loan. A low score signals more risk for the lender.

- Banks look at your score.

- Loan companies look at your score.

- Dealerships look at your score.

A low score doesn’t mean you can’t get a loan. It just means lenders might be more careful. They might ask for more proof you can pay. They might also charge you more to borrow the money.

Reasons for Bad Credit

Many things can cause a low credit score. Life happens.

- Missing bill payments.

- Having too much debt.

- Using too much of your credit card limit.

- Having loans go to collections.

- Bankruptcy.

- Not having much credit history at all.

It’s okay if your credit isn’t perfect. The goal is to show lenders you can handle a new loan, even with past issues.

Learning About Bad Credit Auto Loans

When your credit score is low, usually below 600 or 620, the loans you get are often called subprime auto loans. These loans are for people who don’t qualify for standard loans because of their credit history.

- Subprime means higher risk for the lender.

- Because of the higher risk, these loans usually cost more.

- The interest rate will likely be higher than what someone with good credit pays.

- The total cost of the car will be higher over time.

Even with higher costs, a subprime auto loan can be a step towards better credit. Making on-time payments helps rebuild your score.

Finding Bad Credit Auto Lenders

So, where do you look for a car loan when your credit is not great? You have a few options. It’s wise to check more than one place. This helps you compare offers.

- Banks: Your local bank or credit union might offer loans. They may be stricter but sometimes offer better rates if you’re already a customer.

- Credit Unions: These are non-profit and can sometimes offer better rates than banks. They might be more willing to work with members who have lower scores.

- Online Lenders: Many companies online specialize in bad credit car loans. They have easy online forms and can give quick answers.

- Dealerships: Many car dealerships for bad credit have relationships with lenders who work with people who have low scores. Some even offer their own financing.

Car Dealerships for Bad Credit

Dealerships can be a good place to start when you want to buy a car with bad credit. They want to sell cars. Many have special finance departments that work with various lenders, including those specializing in auto financing with poor credit.

- They can submit your application to many lenders at once. This saves you time.

- They know which lenders are more likely to approve someone with a low score.

- They might have deals or programs for people rebuilding credit.

Some dealerships are known as “buy here, pay here” lots.

Figuring Out “Buy Here, Pay Here”

Buy here, pay here dealerships are different. When you get a loan from a buy here, pay here place, you are getting the loan directly from the dealership itself.

- The dealership is the lender.

- You make your payments directly to the dealership.

- Approval is often based more on your income than your credit score.

- They are known for guaranteed car finance claims, but be careful.

While they make it easy to get approved, these loans often have very high interest rates. The cars might also be older or have higher mileage. Sometimes, payments might not be reported to credit bureaus. If payments aren’t reported, it won’t help improve your credit score. Always ask if they report payments.

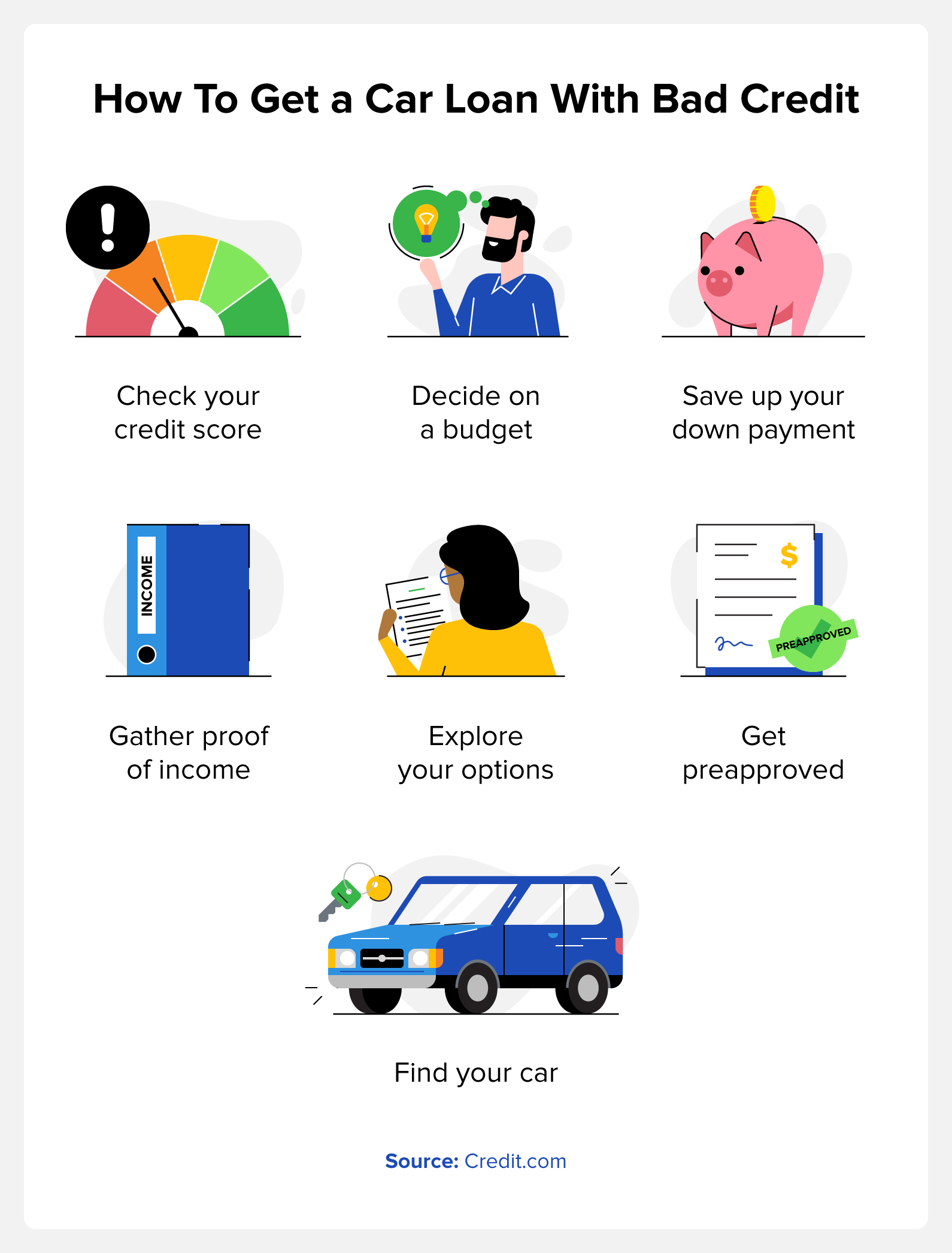

How to Get a Car Loan With Bad Credit

Getting approved requires some steps. It’s not just about finding a lender. It’s about showing you are a good risk now.

Here is a plan to follow:

Step 1: Check Your Credit Report

Before you do anything else, know where you stand. Get copies of your credit report from the three main bureaus: Equifax, Experian, and TransUnion. You can get free reports each year.

- Look for errors. Fix any mistakes you find. This can help your score.

- See which accounts are causing your low score.

Step 2: Figure Out What You Can Afford

Don’t just think about the monthly payment. Think about the total cost.

- How much can you pay each month for the car loan?

- Factor in insurance, gas, maintenance, and registration.

- Lenders look at your debt-to-income ratio (DTI). This is how much of your monthly income goes to paying debts. A lower DTI is better.

- Use a simple budget calculator.

Step 3: Save for a Down Payment

This is a big one. A down payment helps a lot when you have bad credit.

- It lowers the amount you need to borrow.

- It lowers your monthly payment.

- It shows lenders you are serious and have some money saved.

- It reduces the lender’s risk.

Aim for at least 10-20% of the car’s price if you can. Even a small down payment is better than none.

Step 4: Think About a Co-signer

A co-signer is someone with good credit who signs the loan with you. They promise to pay the loan if you can’t.

- This lowers the risk for the lender.

- It can help you get approved.

- It might get you a better interest rate.

Be careful with a co-signer. If you miss payments, it hurts their credit too. It can damage your relationship. Make sure you can make the payments on your own.

Step 5: Get Pre-Approved

Getting pre-approved means a lender checks your credit and income and tells you how much they might loan you.

- It gives you a clear budget before you shop.

- It lets you compare offers from different lenders.

- It’s usually a “soft” credit check at first, which doesn’t hurt your score.

Getting pre-approved puts you in a stronger position at the dealership. You know your loan terms before you even pick a car.

Step 6: Shop Around (for Loans and Cars)

Don’t take the first offer you get. Compare loan terms from different bad credit auto lenders.

- Look at the interest rate (APR).

- Look at the loan term (how many months to pay it back).

- Look at the total cost of the loan.

Once you have loan offers, then find a car that fits your budget and loan amount. Some lenders might have rules about the age or mileage of the car.

Step 7: Be Ready to Negotiate

When you go to the dealership, you can negotiate the car’s price. Knowing your loan terms already helps.

- Negotiate the car price first, separate from the loan.

- Don’t feel pressured to take dealership financing if you have a better offer.

- Be ready to walk away if the deal isn’t right.

Step 8: Read Everything Carefully

Before you sign any papers, read the loan contract.

- Check the interest rate.

- Check the monthly payment.

- Check the total loan amount.

- Look for any extra fees or add-ons.

Ask questions if you don’t understand something.

Improving Your Chances of Getting Approved

Beyond the steps above, here are more tips for getting approved for a car loan bad credit.

- Prove Your Income: Lenders need to know you can pay. Bring pay stubs, tax returns, or bank statements.

- Show Stability: If you’ve been at the same job or lived at the same address for a while, it helps. Lenders like to see you are settled.

- Explain Past Problems: Be honest with the lender if there’s a clear reason for past credit issues (like job loss or medical bills). Show how things are better now.

- Have Proof of Residence: Bring utility bills or bank statements with your current address.

- Bring References: Some lenders might ask for personal references.

- Consider a Less Expensive Car: A lower-priced car means a smaller loan, which is easier for lenders to approve with bad credit.

Learning About Subprime Auto Loans Costs

As mentioned, subprime auto loans come with higher costs. It’s important to know how this impacts you.

- Higher Interest Rates: The interest rate is the cost of borrowing money. With bad credit, your rate might be 10%, 15%, or even higher. Someone with good credit might pay 3-5%.

- Longer Loan Terms: Sometimes, lenders offer longer loan terms (like 60, 72, or even 84 months) to make the monthly payment lower. This sounds good, but you pay more interest over time. The car’s value might also drop below what you owe (being “upside down” on the loan).

- Total Cost: Due to the higher rate and possibly longer term, you will pay much more for the car overall than someone with good credit.

Example Cost Comparison (Illustrative):

Let’s say you borrow $20,000 for a car.

| Feature | Good Credit Example | Bad Credit Example |

|---|---|---|

| Interest Rate (APR) | 5% | 15% |

| Loan Term | 60 months | 60 months |

| Monthly Payment | ~$377 | ~$476 |

| Total Paid Back | ~$22,600 | ~$28,560 |

| Total Interest Paid | ~$2,600 | ~$8,560 |

(Note: These are simple examples. Real loan costs vary based on exact terms and fees.)

This table shows how a higher interest rate significantly increases your monthly payment and the total amount you pay back.

Decoding “Guaranteed Car Finance”

You might see ads for guaranteed car finance or “no credit check” loans. Be very careful with these.

- No True Guarantee: No lender can truly guarantee you a loan before seeing any information about you. There are always some basic requirements (like proving income).

- High Costs: These loans often have extremely high interest rates and fees.

- Bad Terms: The loan terms might not be good for you.

- Limited Car Choices: You might only be able to choose from a small number of older cars.

Often, “guaranteed” simply means they will approve someone, not necessarily you, or that they approve almost everyone but at a very high price. Always read the fine print carefully.

Buying a Car With Bad Credit: What to Expect at the Dealership

When you visit car dealerships for bad credit, here’s what might happen:

- They will ask you to fill out a credit application.

- They will check your credit score.

- They will ask for proof of income (pay stubs).

- They might ask about your job history and where you live.

- They will send your application to lenders they work with who approve car loans for low credit scores.

- They will show you cars that fit the loan amount you are approved for.

Be prepared for them to focus on the monthly payment. Always look at the total price and the interest rate too. Don’t let them rush you.

Managing Your Loan to Rebuild Credit

Getting a bad credit car loan can be a chance to improve your financial health.

- Make Payments ON TIME, EVERY TIME: This is the most important thing. Late payments hurt your score a lot. Set up reminders or automatic payments.

- Pay More Than the Minimum (if possible): Paying a little extra each month can help you pay off the loan faster and pay less interest.

- Keep the Car Insured: Lenders require you to have full coverage insurance until the loan is paid off. Factor this cost into your budget.

- Understand Your Loan Terms: Know your payment date, interest rate, and payoff amount.

Making timely payments on a car loan that is reported to credit bureaus will help rebuild your credit score over time. This makes future borrowing easier and cheaper.

Alternatives to Auto Financing With Poor Credit

Maybe getting a loan right now isn’t the best step. Are there other ways to get a car?

- Save Up and Pay Cash: This is the cheapest way to get a car. You avoid all interest charges. You might have to buy a less expensive car this way, but it can be a smart move.

- Buy a Cheaper Car: Instead of trying to finance a new car with bad credit, maybe a reliable used car that costs less is a better fit for your budget right now.

- Use Public Transport or Carpool: If possible, waiting to buy a car while you save up and improve your credit might be an option.

Pros and Cons of Bad Credit Car Loans

We have talked about how it’s possible, but let’s look at the good and bad points.

Pros:

- You can get a car you need for work or family.

- Making on-time payments can help you rebuild your credit score.

- It might be your only option for a car right now.

- Having a car can help you get to a better job or handle daily life better.

Cons:

- Higher interest rates mean the loan costs you a lot more money.

- Monthly payments can be high.

- You might be limited to certain types of cars or older models.

- You could end up owing more than the car is worth.

- Missing payments can severely damage your credit even more.

- Predatory lenders exist; you need to be careful and research.

Final Thoughts on Getting Approved for a Car Loan Bad Credit

Getting a car when you have bad credit is possible, but it requires smart steps. Don’t rush into the first offer. Do your homework.

- Check your credit report.

- Know your budget.

- Save for a down payment.

- Compare offers from different bad credit auto lenders.

- Be careful at car dealerships for bad credit, especially buy-here-pay-here lots.

- Understand the terms of the subprime auto loan.

- Make your payments on time to rebuild your credit.

Taking the right steps can help you get the car you need and work towards a better financial future.

Frequently Asked Questions (FAQ)

h4 How quickly can I get a car loan with bad credit?

It can happen fairly quickly, sometimes in a day or two if you have all your paperwork ready. Online lenders or dealerships can often give you a fast answer.

h4 What credit score is considered “bad credit” for a car loan?

Generally, a FICO score below 600 or 620 is seen as bad credit. However, lenders have different rules. Some might approve scores slightly lower.

h4 How much down payment do I need with bad credit?

There is no set amount, but a larger down payment is always better. Aim for at least 10% if possible. Some lenders might require more, especially for lower scores or higher loan amounts.

h4 Will applying for multiple loans hurt my credit score more?

If you apply for several car loans within a short time (usually about 14-45 days), credit bureaus count them as one inquiry. This has a small effect on your score. It is better to apply for a few loans in a short window than spread out over months.

h4 Can I get a car loan with no credit history?

Yes, this is possible but can be similar to having bad credit. Lenders have no information to judge your risk. You might need a co-signer or need to put down a larger down payment. Some lenders have programs for first-time buyers.

h4 What interest rate should I expect with bad credit?

Rates vary a lot based on your exact score, income, loan amount, and the car. You might see rates anywhere from 8% to over 20%. This is much higher than rates for good credit.

h4 Are there special programs for people with bad credit?

Some lenders or dealerships might have specific programs for people with low scores or past credit problems. These are often the bad credit auto lenders or finance companies that partner with dealerships. Ask if they have special finance options.

h4 What is a reasonable car price when I have bad credit?

Focus on what you can afford each month, including all car costs (loan, insurance, gas, repairs). It is often wise to buy a reliable used car that costs less to keep the loan amount smaller and more manageable.

h4 Can I refinance a bad credit car loan later?

Yes! If you make your payments on time for 6-12 months and your credit score improves, you might be able to refinance the loan. This means getting a new loan with a lower interest rate from a different lender. This can save you a lot of money.